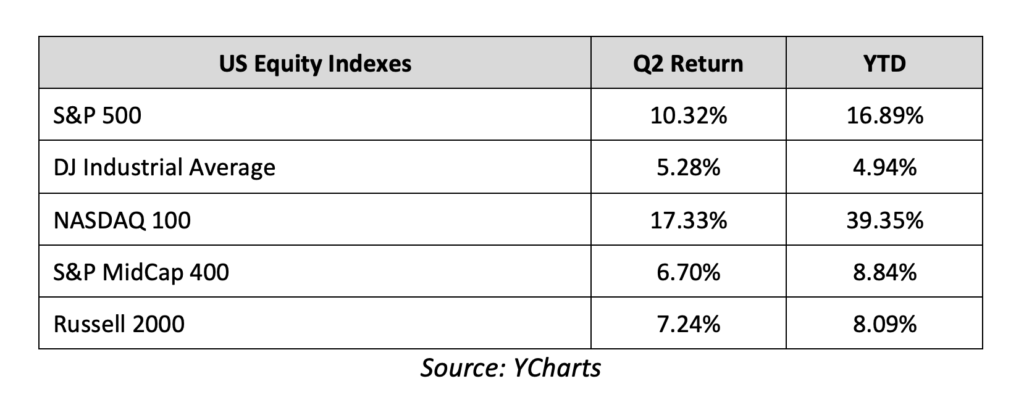

The S&P 500 ended the first half of 2023 at a 14-month high and most major stock indices logged solid gains in the second quarter following a pause in the Fed’s rate hike campaign, stronger-than-expected corporate earnings (especially in the tech sector) and the relatively drama-free resolution of the debt ceiling.

The second quarter began with markets still in the throes of the regional bank crisis following the March failures of Silicon Valley Bank and Signature Bank, and investors started the month of April wary of contagion risks. Those concerns proved mostly overdone, however, as throughout most of the month regional banks were stable. That stability allowed investors to re-focus on corporate earnings, and the results were much better than feared as 78% of S&P 500 companies reported better-than-expected Q1 earnings, a number solidly above the 66% long-term average. Additionally, 75% of reporting companies beat revenue estimates for the first quarter, also well above the long-term average. That solid corporate performance was a welcome sight for investors and coupled with general macroeconomic calm, allowed stocks to drift steadily higher throughout most of April. However, following an underwhelming earnings report, concerns about the solvency of First Republic Bank weighed on markets late in the month and the S&P 500 declined into the end of April to finish with a modest gain.

Fears of a First Republic Bank failure were realized on May 1st, as the bank was seized by regulators and the FDIC was appointed its receiver. However, that same day, JPMorgan announced it was acquiring the bank from the FDIC, and that move helped to calm investor anxiety about financial contagion risks. The Federal Reserve also helped to distract investors from the First Republic failure, as the Fed hiked rates at the May 2nd FOMC meeting, but importantly altered language in the statement to imply it would pause rate hikes at the next meeting. That change was expected by investors, however, and as such it failed to ignite a meaningful rally in stocks. Instead, the tech sector helped push the S&P 500 higher in mid-May, thanks to an explosion of investor and financial media enthusiasm around Artificial Intelligence (AI), which was highlighted by a massive rally in Nvidia (NVDA) following a strong earnings report. However, like in April, the end of the month saw an increase in volatility. This time it was thanks to the lack of progress on a U.S. debt ceiling extension and rising fears of a debt ceiling breach and possible U.S. debt default. However, a two-year debt ceiling extension was agreed to by Speaker McCarthy and President Biden on May 28th and was signed into law a few days later, avoiding a financial calamity. The S&P 500 finished May with a slight gain.

With the debt ceiling resolved, a Fed pause in rate hikes expected and continued stability in regional banks, the rally in stocks resumed in early June and was aided by several potentially positive developments. First, inflation declined as the Consumer Price Index (CPI) hit the lowest level in two years. Second, economic data remained impressively resilient, reducing fears of a near-term recession. Finally, in mid-June, the Federal Reserve confirmed market expectations by pausing rate hikes and that helped fuel a broad rally in stocks that saw the S&P 500 move through 4,400 and hit the highest levels since April 2022. The last two weeks of the month saw some consolidation of that rally thanks to mixed economic data, political turmoil in Russia and hawkish rhetoric from global central bankers, but the S&P 500 still finished June with strong gains.

In sum, markets were impressively resilient in the second quarter and throughout the first half of 2023, as better-than-feared earnings, expectations for less-aggressive central bank rate hikes, more evidence of a “soft” economic landing and relative stability in the regional banks pushed the S&P 500 to a 14-month high.

Second Quarter Performance Review

The second quarter of 2023 saw an acceleration of the tech sector outperformance witnessed in the first quarter, as “AI” enthusiasm drove several mega-cap tech stocks sharply higher. Those strong gains resulted in large rallies in the tech-focused Nasdaq and, to a lesser extent, the S&P 500 as the tech sector is the largest weighted sector in that index. Also like in the first quarter, the less-tech-focused Russell 2000 and Dow Industrials logged more modest, but still solidly positive, quarterly returns.

By market capitalization, large caps outperformed small caps, as they did in the first quarter of 2023. Regional bank concerns and higher interest rates still weighed on small caps as smaller companies are historically more dependent on financing to maintain operations and fuel growth.

From an investment style standpoint, growth handily outperformed value again in the second quarter, continuing the sharp reversal from 2022. Tech-heavy growth funds benefited from the aforementioned “AI” enthusiasm. Value funds, which have larger weightings towards financials and industrials, relatively underperformed growth funds, as the performance of non-tech sectors more reflected the broad economic reality of mostly stable, but unspectacular, economic growth.

On a sector level, eight of the 11 S&P 500 sectors finished the second quarter with positive returns. As was the case in the first quarter, the Consumer Discretionary, Technology, and Communication Services sectors were the best performers for the quarter. The surge in many mega-cap tech stocks such as Amazon (AMZN), Apple (AAPL), Alphabet (GOOGL), Meta Platforms (META), and Nvidia (NVDA) drove the gains in those three sectors, and they handily outperformed the remaining eight S&P 500 sectors. Industrials, Financials, and Materials saw moderate gains over the past three months, thanks to rising optimism regarding a “soft” economic landing.

Turning to the laggards, traditional defensive sectors such as Consumer Staples and Utilities declined slightly over the past three months, as resilient economic data caused investors to rotate to sectors that would benefit from stronger than expected economic growth. Energy also posted a slightly negative return for the second quarter, thanks to weakness in oil prices.

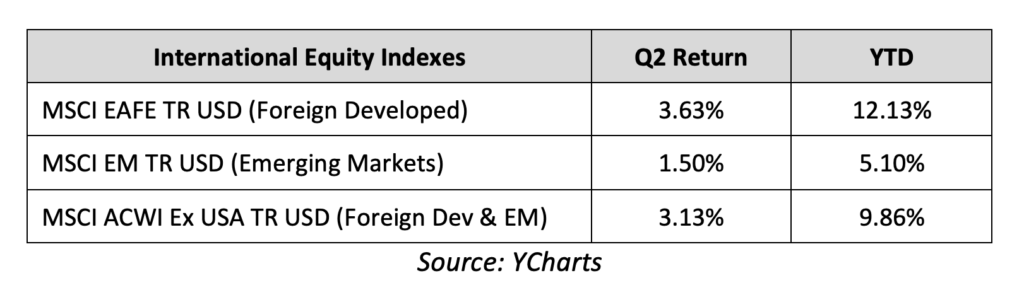

Internationally, foreign markets lagged the S&P 500 due mostly to the relative lack of large-cap “AI” exposed stocks in major foreign indices, combined with some late-quarter worries about the EU economy and pace of Bank of England rate hikes, although foreign markets did finish the second quarter with a modestly positive return. Foreign developed markets outperformed emerging markets thanks to a lack of significant economic stimulus in China, which weighed on emerging markets late in the quarter.

The leading benchmark for bonds (Bloomberg Barclays US Aggregate Bond Index) realized a slightly negative return for the second quarter of 2023, as the resilient economy and hope of a near-term end to Fed rate hikes led investors to embrace riskier assets. Looking deeper into the fixed income markets, shorter-duration bonds outperformed those with longer durations in the second quarter, as bond investors priced in a near-term end to the Fed’s rate hike campaign, while optimism regarding economic growth caused investors to rotate out of the safety of longer-dated fixed income. In the corporate bond market, lower-quality, but higher-yielding “junk” bonds rose modestly in the second quarter while higher-rated, investment-grade debt logged only a slight gain. That performance gap reflected investor optimism on the economy, which led to taking more risk in exchange for a higher return.

Third Quarter Market Outlook

As we begin the third quarter of 2023, the outlook for stocks and bonds is arguably the most positive it’s been since late 2021, as inflation hit a two-year low, economic growth and the labor market remain impressively resilient, the Fed has temporarily paused its historic rate hiking campaign, the debt ceiling extension is resolved, and we’ve seen no significant contagion from the regional bank failures from earlier this year.

That improvement in the fundamental outlook has been reflected in both stock and bond prices so far this year, as the S&P 500 hit the best levels since last April and more cyclically focused sectors led markets higher late in the quarter on rising hopes for a broad economic expansion.

However, while clearly the past quarter brought positive developments in the economy and the markets, leading the financial media to proclaim a “new bull market” has started, it’s important to remember that potentially significant risks remain to the economy and markets. Put more bluntly, the market has taken a decidedly positive view on the ultimate resolution of multiple macroeconomic unknowns, but their outcomes remain very uncertain and thanks to the strong year-to-date rally in stocks, there is now little room for disappointment.

First, the economy has not yet felt the full impact of the Fed’s historically aggressive hike campaign, and while the economy has proved surprisingly resilient so far, we know from history that the impacts of rate hikes can take far longer than most expect to impact economic growth. Put in plain language, it’s premature to think the economy is “in the clear” from recession risks, and we should all expect the economy to slow more as we move into the second half of 2023. The key for markets will be the intensity of that slowing, as at these valuation levels stocks are not pricing in a significant economic slowdown.

On inflation, clearly there’s been progress in bringing inflation down, as year-over-year CPI has fallen from over 9% in 2022 to 4% in less than a year’s time. However, even at 4%, CPI remains far above the Fed’s 2% target. If inflation bounces back, or fails to continue to decline, then the Fed could easily hike rates further, like the Bank of Canada and Reserve Bank of Australia did in the second quarter, following pauses of their own. Those higher rates would weigh further on economic growth.

Turning to banks, markets have taken the regional bank failures in stride, as the collapse of First Republic Bank caused minimal volatility in the second quarter. However, it’s likely premature to consider the crisis “over” and at a minimum, reduced lending by regional banks poses an additional threat to the commercial real estate market and small businesses more broadly. Bottom line, measures taken by the Fed in March have “ringfenced” the regional bank stress for now, but this remains a risk to the economy.

Finally, markets are trading at their highest valuation in over a year, and investor sentiment has turned suddenly, and intensely, optimistic. The CNN Fear/Greed Index ended the second quarter at “Extreme Greed” levels, while the American Association for Individual Investors (AAII) Bullish/Bearish Sentiment Index hit the most bullish level since November 2021, right before the market collapse started in early 2022. Positive sentiment does not automatically mean markets will decline, but the sudden burst of enthusiasm needs to be considered in the context of what is a still uncertain macroeconomic environment and markets no longer have the protection of low expectations and valuations to cushion declines.

In sum, clearly there have been positive macro developments so far in 2023 that have helped the stock market rebound. However, it’s important to remember that multiple and varied risks remain for the economy and markets.

While we are happy with the market’s performance, we remain vigilant towards economic and market risks and are focused on managing both risk and return potential. We understand that a well-planned, long-term-focused, and diversified financial plan can withstand virtually any market surprise and related bout of volatility, including bank failures, multi-decade highs in inflation, high interest rates, geopolitical tensions, and rising recession risks.

We understand the risks facing both the markets and the economy. Recent volatility is unlikely to alter a diversified approach set up to meet your long-term investment goals. A diversified approach will be based on a portfolio allocation that considers your financial position, risk tolerance, and investment timeline. It’s important to stay invested, remain patient and stick to your plan.