The S&P 500 rose to the highest level since March 2022 early in the third quarter but rising global bond yields, fears of a rebound in inflation, and concerns about a future economic slowdown weighed on the major indices in August and September and the S&P 500 finished the third quarter with a modest loss.

The S&P 500 started the third quarter largely the same way it ended the second quarter – with gains. Stocks rose broadly in July thanks primarily to “Goldilocks” economic data, meaning the data showed solid economic growth but not to the extent that would have implied the Federal Reserve needed to hike rates further than investors expected. That solid economic data combined with a decline in inflation metrics further boosted stock prices, as investors embraced reduced near-term recession risks and steadily declining inflation. The Federal Reserve, meanwhile, increased interest rates in late July but also signaled that could be the last rate hike of the cycle. That tone and commentary further fueled optimism that one of the most aggressive rate hike cycles in history was soon coming to an end. Finally, Q2 earnings season was better-than-feared with mostly favorable corporate guidance which supported expectations for strong earnings growth into 2024. The S&P 500 rose to the highest level since March 2022 and the index finished with a strong monthly gain of more than 3%.

The market dynamic changed on the first day of August, however, when Fitch Ratings, one of the larger U.S. credit rating agencies, downgraded U.S. sovereign debt. Fitch cited long-term risks of the current U.S. fiscal trajectory as the main reason for the downgrade, but while that lacked any near-term specific justification for the downgrade, the action itself put immediate downward pressure on U.S. Treasuries, sending their yields meaningfully higher. The Fitch downgrade kickstarted a rise in Treasury yields that lasted the entire month, as the downgrade combined with a rebound in anecdotal inflation indicators and a large increase in Treasury sales stemming from the debt ceiling drama pushed yields sharply higher. The 10-year Treasury yield rose from 4.05% on August 1st to a high of 4.34% on August 21st, the highest level since mid-2007. That rapid rise in yields weighed on stock prices throughout August and the S&P 500 posted its first negative monthly return since February, as higher rates pressured equity valuations and raised concerns about a future economic slowdown. The S&P 500 finished August down 1.59%.

The August volatility subsided in early September, however, as solid economic data and a pause in the rise in Treasury yields allowed the S&P 500 to stabilize through the first half of the month. But volatility returned following the September Fed decision as the FOMC delivered markets a “hawkish” surprise, despite not increasing interest rates. Specifically, the majority of Fed members reiterated that they anticipated the need for an additional rate hike before the end of the year and forecasted only two rate cuts for all of 2024, down from four rate cuts forecasted at the June meeting. Then, late in the month, two additional developments weighed further on both stocks and bonds. First, the United Auto Workers labor union began a general strike, a move that would disrupt automobile production and temporarily weigh on economic growth. Second, the U.S. careened towards another government shutdown as Republicans and Democrats failed to agree on a “Continuing Resolution” to fund the government. The shutdown was avoided at the last minute, but the funding extension only lasts until November 17th meaning there will likely be another budget battle in the coming months. The S&P 500 declined towards the end of the month to hit a fresh three-month low, ending September down modestly.

In sum, volatility returned to markets during the third quarter, as rising bond yields pressured stock valuations, some inflation indicators pointed to a bounce back in inflation and the Fed reiterated a “higher for longer” interest rate outlook.

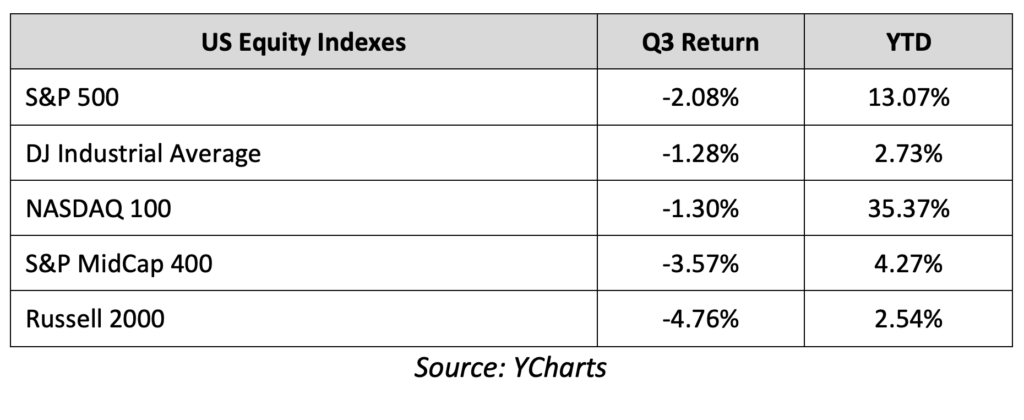

Third Quarter Performance Review

Rising bond yields were the main driver of the markets in the third quarter as high Treasury yields caused reversals in performance on a sector and index basis, relative to the first and second quarters.

Starting with market capitalization, large caps once again outperformed small caps, as they did in the first two quarters of 2023, although both posted negative returns. That relative outperformance by large caps is consistent with rising Treasury yields, as smaller companies are typically more reliant on debt financing to sustain operations and rising interest rates create stronger financial headwinds for smaller companies when compared to their larger peers.

From an investment style standpoint, however, we did see a performance reversal from the first two quarters of the year as value relatively outperformed growth in the third quarter, although both investment styles finished with a negative quarterly return. Rising bond yields tend to weigh more heavily on companies with higher valuations and since most growth funds overweight higher P/E tech stocks, those funds lagged last quarter. Value funds that include stocks with lower P/E ratios are less sensitive to higher yields, and as such, they outperformed in the third quarter.

On a sector level, nine of the 11 S&P 500 sectors finished the third quarter with a negative return, which is a stark reversal from the broad gains of the second quarter. Energy was, by far, the best-performing S&P 500 sector in the third quarter thanks to a surge in oil prices. Communications Services also finished Q3 with a slightly positive quarterly return on hopes integration of advanced artificial intelligence would boost search and social media companies’ future advertising revenues.

Looking at sector laggards, the impact of rising bond yields was again clearly visible as consumer staples, utilities, and real estate were the worst-performing sectors in the third quarter. Those sectors offer some of the highest dividend yields in the market, but with bond yields quickly rising those dividend yields become less attractive and investors rotated out of the high-dividend sectors and into less-volatile bond funds as a result.

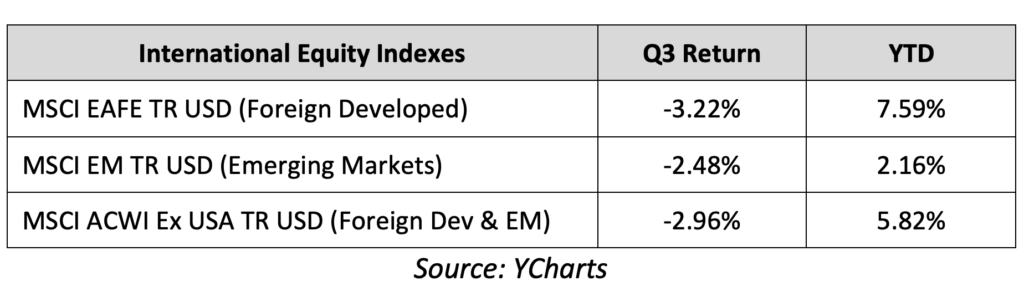

Internationally, foreign markets saw moderate declines and again lagged the S&P 500 in the third quarter as disappointing economic data in Europe and China bolstered regional recession fears. Emerging markets did relatively outperform developed markets, however, thanks to the announcement of larger-scale Chinese economic stimulus late in the quarter.

The leading benchmark for bonds (Bloomberg Barclays US Aggregate Bond Index) declined moderately for a second consecutive quarter as hawkish Fed rhetoric and hints of a rebound in inflation weighed broadly on fixed-income markets. Shorter-duration debt securities posted a positive quarterly return and outperformed those with longer durations in the third quarter, as the Fed did not signal it intended to raise interest rates any higher than previously expected. Longer-duration bonds, however, were pressured by the combination of a rebound in some inflation indicators and as investors digested that the Fed may well delay any rate cuts in 2024, keeping rates “higher for longer.” In the corporate bond market, lower-quality but higher-yielding “junk” bonds rose slightly while higher-rated, investment-grade debt declined moderately in Q3. The large performance gap reflected continued optimism from investors regarding future economic growth, as investors “reached” for higher yields offered by riskier companies amidst broadly rising bond yields.

Fourth Quarter Market Outlook

Markets begin the fourth quarter decidedly more anxious than they started the third quarter, but it’s important to realize that while the S&P 500 did hit multi-month lows in September and there are legitimate risks to the outlook, underlying fundamentals remain generally strong.

First, while there are reasonable concerns about a future economic slowdown, the latest economic data remains solid. Employment, consumer spending and business investment were all resilient in the third quarter and there simply isn’t much actual economic data that points to an imminent economic slowdown. So, while a future economic slowdown is certainly possible given higher interest rates, the resumption of student loan payments and declining U.S. savings, the actual economic data is clear: It isn’t happening yet.

Second, fears that inflation may bounce back are also legitimate, given the rally in oil prices in the third quarter. But the Federal Reserve and other central banks typically look past commodity-driven inflation and instead focus on “core” inflation and that metric continued to decline throughout the third quarter. Additionally, declines in housing prices from the recent peak are only now beginning to work into the official inflation statistics, and that should see core inflation continue to move lower in the months and quarters ahead.

Finally, regarding monetary policy, the Federal Reserve’s historic rate hike campaign is nearing an end. And while we should expect the Fed to keep rates “higher for longer,” high-interest rates do not automatically result in an economic slowdown. Interest rates have merely returned to levels that were typical in the 1990s and early 2000s, before the financial crisis, and the economy performed well during those periods. The risk of higher rates causing an economic slowdown is one that must be monitored closely, but for now, higher rates are not causing a material loss of economic momentum.

In sum, there are real risks to both the markets and the economy as we begin the final three months of the year. But these are largely the same risks that markets have faced throughout 2023 and over that period the economy and markets have remained impressively resilient. So, while these risks and others must be monitored closely, they don’t present any new significant headwinds on stocks that haven’t existed for much of the year.

That said, as we begin the final quarter of 2023, we remain vigilant toward economic and market risks and are focused on managing both risk and return potential. We remain firm believers that a well-prepared, long-term-focused, and diversified financial plan can withstand virtually any market surprise and related bout of volatility, including “higher for longer” interest rates, stubbornly high inflation, geopolitical tensions, and recession risks.

We understand the risks facing both the markets and the economy. Recent volatility is unlikely to alter a diversified approach set up to meet your long-term investment goals. A diversified approach will be based on a portfolio allocation that considers your financial position, risk tolerance, and investment timeline. It’s important to stay invested, remain patient, and stick to your plan.

Thank you for your ongoing confidence and trust. Please rest assured that we remain dedicated to helping you successfully navigate this market environment.