Markets staged an impressive reversal in the fourth quarter thanks to a surprise dovish pivot by the Federal Reserve, which combined with solid economic activity and declining inflation to push stocks sharply higher and send the S&P 500 to two-plus-year highs, resulting in the best annual return since 2021.

The strong fourth quarter performance somewhat obscures the fact that stocks and bonds started the fourth quarter under significant pressure. First, Treasury yields continued to move higher in early October which weighed on stocks and bonds, just like in the third quarter. Then on October 7th, Hamas soldiers infiltrated settlements in Israel, killing and kidnapping more than 1,200 Israelis in the worst attack on Israel in decades. The market fallout was immediate, as oil prices spiked on fears a broader regional war would ensue between Israel, Hamas, Lebanon and, potentially, Iran. Higher oil prices fueled a further increase in Treasury yields as investors priced in a possible oil-driven bounce back in inflation. Those factors, combined with a lackluster earnings season, resulted in the S&P 500 falling to the lowest levels since mid-May while the 10-year Treasury yield touched 5.00% for the first time since the mid-2000s. However, markets reversed when Fed Governor Chris Waller made comments that implied rate hikes were over and rate cuts may be coming in 2024. The market reaction was immediately positive as stocks and bonds rallied hard into month-end to finish well off the lows and with just a 2% decline.

That positive momentum continued in November as the S&P 500 posted its best monthly return of 2023, rising more than 9%. There were several factors that fueled this rally. First, numerous Fed officials echoed Waller’s commentary and investors priced in rate cuts as early as May, substantially earlier than previously expected. Additionally, the Israel/Hamas conflict did not spread and remained contained between Israel and Hamas and oil prices declined as a result, easing inflation concerns. Finally, inflation metrics continued to decline. The year-over-year increase in the Consumer Price Index dropped to 3.14% and that further fueled investor expectations that rate cuts would come in the first half of 2024. Those factors combined with generally favorable seasonality to fuel a welcomed “Santa Claus Rally.”

The Santa rally continued and accelerated in December courtesy of the Fed. At the December 13th FOMC meeting, Fed officials clearly signaled that rate hikes were over and forecasted three rate cuts in 2024, one more than previously forecasted. Additionally, Fed Chair Powell did little to push back against the markets’ expectations for rate cuts. Put plainly, the Fed surprisingly pivoted to a more dovish policy stance and that fueled a continuation of the rally that started in late October. The S&P 500 rose to the highest level since January 2022 while the Dow Industrials hit a new all-time high.

In sum, 2023 was a year of surprises for the markets as the expectations for a recession never materialized, inflation fell faster than forecasts, corporate earnings proved resilient and the Fed surprised markets by pivoting to a more dovish future policy. The result was substantial gains for the major averages.

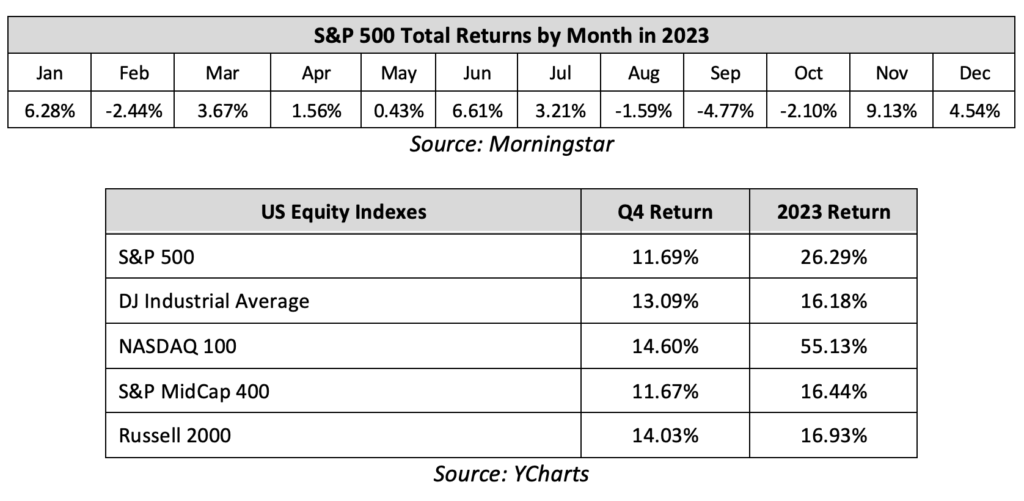

Q4 and Full Year 2023 Performance Review

Stocks enjoyed a broad and powerful rally in the fourth quarter as all four major U.S. stock indices posted strong quarterly gains. Investor expectations for rate cuts in 2024 were a major influence on markets in the fourth quarter as the Russell 2000 and Nasdaq 100 outperformed the S&P 500 over the past three months, as companies in those two indices are expected to benefit most from a sustainable decline in interest rates. For the full year, however, the dual influences of 1) Artificial Intelligence (AI) enthusiasm and 2) Rate cut expectations drove performance as the tech-heavy Nasdaq 100 massively outperformed the other major stock indices, surging more than 50%. The S&P 500 also logged a substantial gain of over 20% thanks mostly to the large weighting of technology stocks in the index. The less-tech-stock-sensitive Dow Industrials and Russell 2000 also enjoyed strong returns in 2023, but relatively underperformed the Nasdaq and S&P 500. Notably, the index performance for the full year 2023 was the opposite of 2022, where we saw the Nasdaq and small caps decline substantially more than the S&P 500 and Dow Jones Industrial Average.

By market capitalization, small caps outperformed large caps in the fourth quarter thanks to those surging rate cut expectations, as lower rates are typically most beneficial for smaller companies. For the full year, however, large caps handily outperformed small caps thanks to the strength in large-cap tech stocks and as the higher rates in the first three quarters of 2023 weighed on small cap performance earlier in the year.

From an investment-style standpoint, growth significantly outperformed value both in the fourth quarter and for the full year. The reasons were familiar ones: Artificial intelligence enthusiasm powered tech-heavy growth funds early in 2023 while in the fourth quarter expectations for rate cuts were seen as positive for growth stocks. Growth outperforming value is also the opposite of 2022, where higher rates and recession fears resulted in value outperforming growth.

On a sector level, 10 of the 11 S&P 500 sectors finished the fourth quarter with a positive return, while eight of the 11 sectors ended 2023 with gains. Not surprisingly, the dual influences of artificial intelligence enthusiasm and expectations for rate cuts drove sector trading in the fourth quarter and throughout the year. In the fourth quarter, the influence of expected lower rates was dominant as REITs were the best performing sector, followed by tech. Both stand to benefit from falling interest rates. Cyclical sectors also outperformed over the past three months as expectations for stable economic growth rose as the Fed telegraphed future rate cuts. For the full year, however, the influence of AI enthusiasm was clearly the dominant influence on sector trading, as the three most “AI sensitive” sectors (tech, consumer discretionary and communications services) massively outperformed the remaining eight S&P 500 sectors.

Looking at sector laggards for the fourth quarter and for the full year, defensive sectors including consumer staples and utilities lagged as economic growth was more resilient than expected while higher rates (for most of 2023) reduced the demand for high dividend yielding sectors. Consumer staples and utilities posted negative returns for 2023 after being the best relative performers in 2022.

Internationally, foreign markets lagged the S&P 500 in the fourth quarter thanks mostly to muted gains in the emerging markets following increased geopolitical tensions in the Middle East and on continued lackluster Chinese economic growth. Foreign developed markets outperformed emerging markets in Q4 on better-than-expected inflation readings and rising expectations other major central banks will follow the Fed’s lead and cut rates in 2024. For the full-year 2023, foreign developed markets registered solidly positive returns but handily underperformed the S&P 500 thanks primarily to the large gains in U.S. tech stocks.

The leading benchmark for bonds (Bloomberg Barclays US Aggregate Bond Index) realized a positive return for the fourth quarter and for the full year as falling inflation and expectations for rate cuts in 2024 pushed bonds higher. Longer-duration bonds outperformed those with shorter durations in the fourth quarter as bond investors reacted to lower-than-expected inflation and priced in future Fed rate cuts. For the full year, however, shorter-duration debt outperformed longer-term bonds as high inflation readings through the first three quarters of 2024 weighed on the long end of the yield curve. Both high yield and investment grade bonds posted sharply positive returns for the fourth quarter as investors embraced the idea of lower interest rates and reduced recession chances. For the full year, high yield corporate bonds posted a very strong return and outperformed investment grade corporate debt as the resilient economy pushed investors to embrace more risk in return for a higher yield.

Q1 and 2024 Market Outlook

At this time last year, the S&P 500 had just logged its worst annual performance since the financial crisis, the Fed was in the midst of the most aggressive rate hike campaign in decades, inflation was above 6% and concerns about an imminent recession were pervasive across Wall Street.

Now, as we begin 2024, the market outlook couldn’t be much more positive. The Fed is done with rate hikes and cuts are on the way, likely in early 2024. Economic growth has proven more resilient than most could have expected and fears of a recession are all but dead. Inflation dropped substantially in 2023 and is not far from the Fed’s target while corporate earnings growth is expected to resume in the coming year.

Undoubtedly, that’s a more positive environment for investors compared to the start of 2023, but just like overly pessimistic forecasts for 2023 proved incorrect, as we look ahead to 2024, we must guard against complacency because at current levels both stocks and bonds have priced in a lot of positives in the new year.

Starting with Fed policy, Fed officials are forecasting three rate cuts in 2024 but investors are currently pricing in six rate cuts in 2024 with the first one occurring in March or May. That’s a very aggressive assumption and if it is incorrect, we should expect an increase in volatility in both stocks and bonds.

Regarding economic growth, it’s foolish to assume just because the economy was resilient in 2023 that it will stay resilient. Obviously, that’s the hope, but hope isn’t a strategy. The longer rates stay high (and they are still high) the more of a drag they create on the economy. Meanwhile, all the remnants of pandemic-era stimulus are gone and there is some economic data that’s starting to point towards reduced consumer spending. Point being, it is premature to believe the economy is “in the clear” and a slowing of growth is something we will be on alert for as we start the new year, because that would also increase market volatility.

Inflation, meanwhile, has declined sharply but it still remains solidly above the Fed’s 2% target. Many investors expect inflation to continue to decline while economic growth stays resilient, a concept traders coined “Immaculate Disinflation.” However, while that’s possible, it’s important to point out it’s extremely rare as declines in inflation are usually accompanied by an economic slowdown.

Finally, corporate earnings have proven resilient but companies are now facing margin compression as inflation declines and economic growth potentially slows. Earnings results and guidance in the fourth quarter were not as strong as earlier in 2023 and if earnings are weaker than expected, that will be another potential headwind on markets.

Bottom line, while undoubtedly the outlook for markets is more positive this year than it was last year, we won’t allow that to breed a sense of complacency because as the past several years have shown, markets and the economy rarely behave according to Wall Street’s expectations.

As such, while we are prepared for the positive outcome currently expected by investors, we are also focused on managing both risks and return potential because the past several years demonstrated that a well-planned, long-term focused and diversified financial plan can withstand virtually any market surprise and related bout of volatility, including multi-decade highs in inflation, historic Fed rate hikes, and geopolitical unrest.

We understand the risks facing both the markets and the economy. Recent volatility is unlikely to alter a diversified approach set up to meet your long-term investment goals. A diversified approach will be based on a portfolio allocation that considers your financial position, risk tolerance, and investment timeline. It’s important to stay invested, remain patient and stick to your plan.