The S&P 500 ended the first quarter of 2023 with a solid gain as hopes for an economic “soft landing” and the Fed signaling that their historic rate hike campaign is coming to an end helped offset two rate increases and the biggest bank failures since the financial crisis.

Markets started 2023 with strong gains in January, which were primarily driven by a continued decline in widely followed inflation indicators. That decline in price pressures was coupled with surprisingly resilient economic data, especially in the labor market. Those forces combined to increase investors’ hopes that the Fed could deliver an economic soft landing, whereby the economy slows but avoids a painful recession while inflation moves close to the Fed’s target. Additionally, corporate earnings for the fourth quarter of 2022, which were reported in January, were “better than feared” and the resilient nature of corporate America contributed to the growing hope that both an economic and earnings recession could be avoided. The S&P 500 posted strong gains in the month of January, rising more than 6%.

In February, growing optimism for an economic soft landing was delivered a setback, however, as economic data implied a still very tight labor market while the decline in inflation stalled. The January jobs report, released in early February, showed a massive gain in jobs, implying that the labor market will remain extremely tight (something the Fed believes is contributing to inflation). Later in the month, widely followed inflation metrics such as CPI and the Core PCE Price Index showed minimal further price declines, implying that the drop in inflation that had powered the gains in stocks was ending. The strong economic data and a leveling off of inflation metrics led investors to price in substantially higher interest rates in the coming months, and that weighed on both stocks and bonds in February. The S&P 500 finished with a modest loss on the month, falling just over 2%.

The final month of the first quarter began with investors still focused on inflation and potential interest rate hikes, but the sudden failure of Silicon Valley Bank, at the time the 16th largest bank in the United States, shifted investor focus to a potentially growing banking crisis. Signature Bank of New York failed just days later, and concerns about a regional banking crisis surged. In response, the Federal Reserve and the Treasury Department created new lending programs aimed at shoring up regional banks and preventing bank runs but concerns about the health of the financial system persisted and those fears weighed on markets through the middle of March. However, while the Federal Reserve hiked interest rates again at the March meeting, policy makers signaled that they are very close to ending the current rate hike campaign. That admission, combined with no additional large bank failures, eased concerns about a growing banking crisis, and the S&P 500 was able to rally during the final two weeks of March to finish the month with a small gain.

In sum, markets were impressively resilient in the first quarter as a looming end to rate hikes, further declines in inflation and quick and effective actions by government officials in response to regional bank failures helped shore up confidence in the banking system. Stocks and bonds both logged modest gains in Q1, despite the threat of a regional banking crisis and still-elevated market volatility.

First Quarter Performance Review

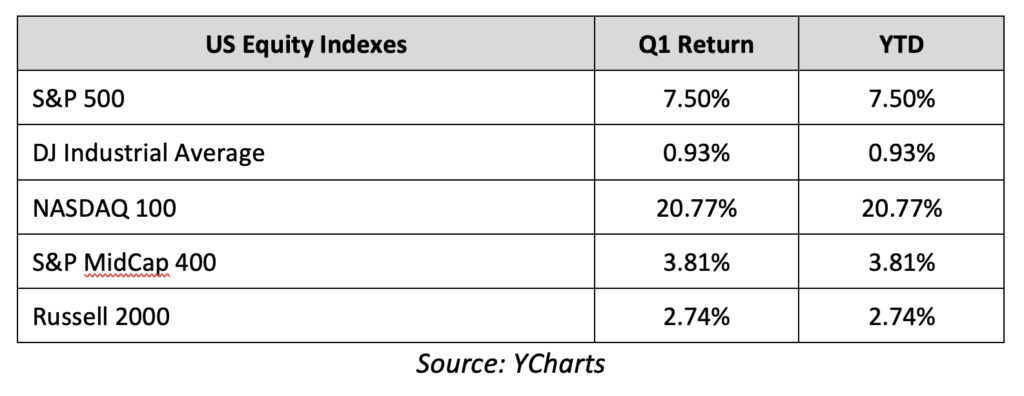

The first quarter of 2023 saw a sharp reversal in index and sector performance compared to 2022. On an index level, the Nasdaq (which badly underperformed in 2022) handily outperformed in the first quarter and finished with very impressive returns. That outperformance was driven by a decline in bond yields (which makes growth-oriented tech and consumer companies more attractive to investors) and mega-cap tech companies such as Apple, Alphabet, Amazon and others viewed as “safe havens” amidst the late-quarter banking stress. The S&P 500, with its heavy weighting to tech, finished the quarter with a solidly positive return while the Dow Industrials and Russell 2000 logged more modest, but still positive returns through the first three months of the year.

By market capitalization, large caps outperformed small caps, as they did throughout 2022. Concerns about funding sources, should the banking crisis worsen, and higher interest rates weighed on small caps as smaller companies are historically more dependent on financing to maintain operations and fuel growth.

From an investment style standpoint, growth handily outperformed value which is a sharp reversal from 2022. Tech-heavy growth funds benefited from the aforementioned decline in bond yields and a late-quarter “flight to safety” amidst the regional banking crisis. Value funds, which have larger weightings towards financials, were weighed down by concerns about a potential broader banking crisis.

On a sector level, seven of the 11 S&P 500 sectors finished the first quarter with a positive return. Notably, the three top performers from the first quarter were the three worst performing sectors in 2022. Communication services was one of the best performing sectors in the first quarter thanks to strong gains from internet-focused tech stocks, as lower rates and the rotation to mega-cap tech companies pushed the sector higher. The technology sector also clearly benefitted from those two trends, as it rose slightly more than the communications sector in Q1. Finally, consumer discretionary, which has larger weightings towards tech-based consumer companies such as Amazon and others, also logged a solidly positive gain thanks to the same general tech stock outperformance and as the labor market remained more resilient than expected, improving the prospects for consumer spending in the months ahead.

Turning to the laggards, the financial sector was the worst performer in the first quarter as the regional banking crisis weighed on bank stocks and financials more broadly. Energy also logged solid declines through the first quarter as growing concerns about global economic growth and subsequent weakness in consumer demand weighed on energy stocks. More broadly, the remaining S&P 500 sectors saw small quarterly gains or losses, as there remains a lot of uncertainty about future economic growth and earnings and the banking stresses that emerged in March will only add an additional headwind on economic growth.

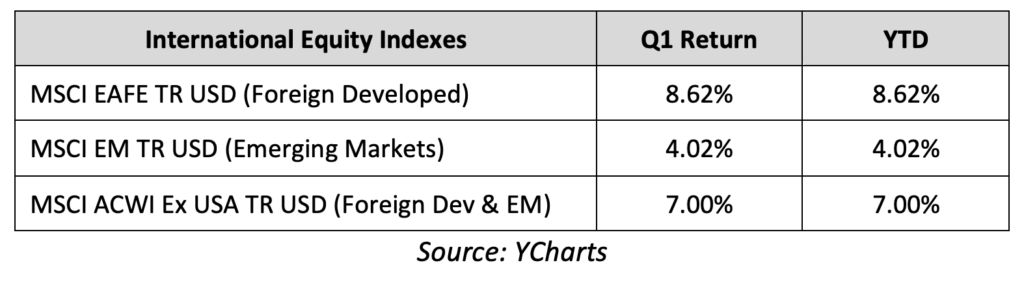

Internationally, foreign markets largely traded in line with the S&P 500 in the first quarter and realized positive returns. Foreign developed markets outperformed the S&P 500 through the first three months of the year as economic data in Europe was better than expected and European banks were viewed as mostly insulated from the U.S. regional bank crisis. Emerging markets logged slightly positive returns through March but underperformed the S&P 500 thanks to still-elevated geopolitical stress, as U.S.-China tensions rose following the Chinese spy balloon affair.

The leading benchmark for bonds (Bloomberg Barclays US Aggregate Bond Index) realized a positive return for the first quarter of 2023, although bonds were volatile to start the year. The Fed signaling an imminent end to rate hikes combined with concerns that the regional banking crisis would raise the odds of a recession, fueled a broad bond market rally in the first quarter. Looking deeper into the fixed income markets, longer-duration bonds outperformed those with shorter durations in the first quarter, as bond investors welcomed further declines in inflation and reached for long-term yield amidst an uncertain outlook for future economic growth. In the corporate bond market, higher-quality investment grade bonds and higher-yielding, “junk” rated corporate debt registered similarly positive returns in the first quarter. Investors moved to both types of corporate debt following declines in inflation and as corporate earnings results were largely better than feared.

Second Quarter Market Outlook

Markets begin the new quarter facing multiple sources of uncertainty including the path of inflation, future economic growth, the number of remaining Fed rate hikes, and whether the regional banking crisis is truly contained. Yet despite all this uncertainty, markets have proven resilient over the past six months since hitting their lows in October of 2022. So, while headwinds remain in place and markets will likely stay volatile, there remains a path for future positive returns.

Starting with the regional banking crisis, despite consistent comparisons in the financial media between what happened in March and the 2007-2008 financial crisis, there are important differences between the two periods and regulators have already demonstrated their commitment to ensuring we do not experience a repeat of those difficult days. As we begin the new quarter, there is reason for hope this crisis has been contained. But regardless of whether that’s true, regulators and government officials have proven they are ready to use current tools (or create new ones) to prevent a broader spread of the regional banking crisis, and that’s an important, and positive, difference from 2008.

Looking past the regional bank crisis, inflation remains a major longer-term influence on the markets and the economy, and whether inflation resumes its decline this quarter will be very important for investors and the markets. More specifically, the decline in inflation somewhat stalled in February and March but if the decline in inflation resumes in the second quarter that will provide a powerful tailwind for both stocks and bonds.

Regarding economic growth, markets rallied on the hope of an economic soft landing earlier in the first quarter, and while the regional banking crisis complicates that optimistic outlook, it is still possible. To that point, employment, consumer spending and economic growth more broadly have remained impressively resilient, so while we should all expect some slowing in the economy this quarter, a recession is by no means guaranteed. If the economy achieves a soft landing that will be a material positive for risk assets.

Finally, after one of the most intense interest rate hike campaigns in history, the Fed has signaled that it is close to being done with rate increases, and that will remove a material headwind on the economy. As long as that expectation for a looming end to rate hikes does not change, it’ll increase the chances that the economy can achieve the desired soft landing.

To be sure, this remains a tumultuous time in the markets. Investors are facing the highest interest rates in decades, the worst geopolitical tensions in years, and a very uncertain economic outlook that deteriorated in the wake of recent bank failures. But while concerning, it’s important to realize that underlying U.S. economic fundamentals and U.S. corporate earnings proved incredibly resilient through the first quarter. And those two factors, steady economic growth and strong earnings, are the real long-term drivers of market performance, not the latest disconcerting geopolitical or financial headlines.

As such, we are prepared for continued volatility and are focused on managing both risks and return potential. We understand that a well-planned, long-term-focused, and diversified financial plan can withstand virtually any market surprise and related bout of volatility, including bank failures, multi-decade highs in inflation, high interest rates, geopolitical tensions, and rising recession risks.

We understand the risks facing both the markets and the economy, and we are committed to helping you effectively navigate this challenging investment environment. Recent volatility is unlikely to alter a diversified approach set up to meet your long-term investment goals. A diversified approach will be based on a portfolio allocation that considers your financial position, risk tolerance, and investment timeline. It’s important to stay invested, remain patient and stick to your plan.