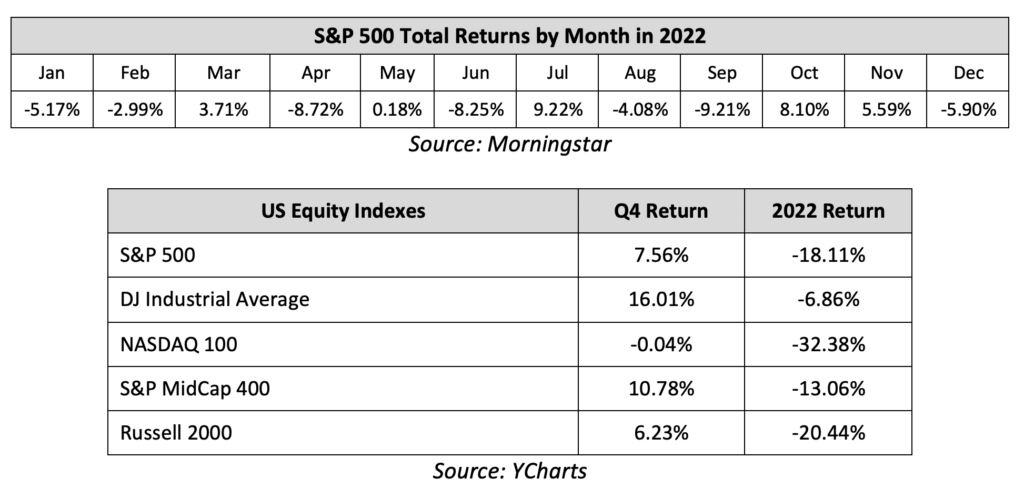

Easing inflation pressures and a resolution of the fiscal turmoil in the United Kingdom fueled a strong rally in stocks and bonds early in the fourth quarter, but hawkish Fed guidance, disappointing economic data, and rising global bond yields weighed on markets in December and the S&P 500 finished the fourth quarter with only modest gains that capped the worst year for the index since 2008.

The end of the third quarter was volatile as global bond yields spiked in response to the spending and tax cut package proposed by former U.K. Prime Minister Liz Truss, and that volatility continued as the fourth quarter began with the S&P 500 hitting a new low for the year on October 13th. However, that market turmoil ultimately resulted in political change in the U.K. as PM Truss resigned on October 20th and was replaced by former Chancellor of the Exchequer Rishi Sunak, who immediately took steps to disavow Truss’ plan and restore market confidence in U.K. finances. In part due to a very short-term oversold condition and following a no-worse-than-feared third-quarter earnings season, stocks and bonds staged large rallies in mid and late October and the S&P 500 finished the month with a substantial gain, rising 8.1%.

The positive momentum for stocks and bonds continued in early November thanks to a growing number of price indicators that implied inflation pressures had finally peaked. The October CPI report (released November 10th) showed the first solid decline in consumer price data for the year and that was echoed by price indices contained in national and regional manufacturing reports, as well as other official inflation statistics. Both stocks and bonds enjoyed solid gains in response to the data because while inflation remained far too high on an absolute level, markets hoped these declines would result in the Federal Reserve not raising interest rates as high as previously feared. Those hopes were boosted after the Thanksgiving holiday when Fed Chair Powell stated that interest rates would only need to rise “somewhat” higher than previous projections. Investors took that “somewhat” remark as a sign that previous estimates for rate hikes were too aggressive and that extended the rally into early December. The S&P 500 ended November at multi-month highs with another solid monthly gain of 5.6%.

However, investor optimism faded in December as global central banks signaled that they were still committed to aggressively hiking rates, economic data showed clear signs of slowing growth, and several negative earnings announcements raised concerns of an earnings recession in 2023. First, at the December meeting, the Fed revealed that they expected rate hikes to take the fed funds rate above 5% (from the current 4.375%), which was higher than market expectations. Then, economic data released in mid-December, including regional manufacturing indices and the November retail sales report, showed economic activity was slowing. Finally, both the European Central Bank and the Bank of Japan surprised markets with hawkish policy decisions, providing yet another reminder to investors that rates will continue to rise in 2023 despite clearly slowing global economic growth and the increasing threat of recession. Stocks dropped from mid-December on, and the S&P 500 ended the month of December with a loss of 5.90%. In sum, 2022 was the most difficult year for investors from a return and volatility standpoint since the Global Financial Crisis. Multi-decade highs in inflation combined with historically aggressive Fed rate hikes and growing concerns about economic and earnings recessions to pressure both stocks and bonds. The S&P 500 posted its worst performance since 2008 while major benchmarks for both stocks and bonds declined together for the first time since the 1960s, punctuating just how disappointing the year was for investors.

Q4 and Full Year 2022 Performance Review

Unlike the first three quarters of 2022, when all four major indices saw quarterly declines, performance was mixed during the fourth quarter as the Dow Jones Industrial Average rose sharply, while the S&P 500 and Russell 2000 were solidly higher. Like most of 2022, however, the Nasdaq lagged and fell slightly in the fourth quarter. Expectations for higher rates, slowing economic growth and underwhelming earnings weighed on the tech sector in the fourth quarter, which was the case for much of 2022. Conversely, less economically sensitive companies that trade at lower valuations than tech stocks outperformed again as investors continued to shift towards defensive sectors amid growing recession fears. On a full-year basis, all four major indices posted negative returns, with the Dow Jones Industrial Average relatively outperforming while the Nasdaq badly lagged the other major indices.

By market capitalization, large-caps slightly outperformed small-caps in the fourth quarter, but modestly outperformed throughout 2022. Concerns about future economic growth and higher interest rates (which can impact small-caps disproportionately due to funding needs) were the main drivers of large-cap outperformance and small-cap underperformance throughout 2022. Small-cap stocks did show some resilience in the fourth quarter with the Russell 2000 index registering a solid gain as investors’ hopes for a peak in inflation and ultimately interest rates, led to some dip buying in the segment.

From an investment style standpoint, value massively outperformed growth all year and that trend continued in the fourth quarter. Underwhelming earnings weighed on tech stocks in the final three months of the year, while concerns about slowing economic growth combined with rising bond yields hit richly valued tech stocks throughout 2022. Value stocks, meanwhile, were viewed as more attractive in the market environment of 2022 due to lower valuations and exposure to business sectors that are considered more resilient than high-growth parts of the market.

On a sector level, 10 of the 11 S&P 500 sectors finished the fourth quarter with a positive return, although only two of the 11 ended 2022 with gains. Energy outperformed other sectors not just in the fourth quarter but for all of 2022. In the fourth quarter, energy stocks were helped by progress on the post-Covid economic reopening in China which increased energy demand expectations, while a falling dollar was an added tailwind for commodities including oil and gas. More to that point, the other strong sector performers in the fourth quarter were industrials and materials, which also benefitted from an improving Chinese demand outlook and a weaker U.S. dollar. For the full year, energy was, by far, the best-performing sector in the market as an early-year surge in oil and natural gas prices in response to increased geopolitical risks and reduced Russian supply helped push energy stocks sharply higher. Defensive sectors, specifically utilities and consumer staples, were the next best-performing sectors finishing the year with small gains and losses, respectively, again as investors rotated towards less economically sensitive corners of the market amid rising recession risks.

The tech sector and those sectors with overweight exposure to high-growth companies badly lagged in the fourth quarter and over the course of 2022. In the fourth quarter, communication services were only fractionally positive while the consumer discretionary sector posted a negative return on weakness in high-growth internet and consumer stocks. For the full year, those same two sectors posted the worst returns in the S&P 500, as investors shunned richly valued, growth-oriented tech companies.

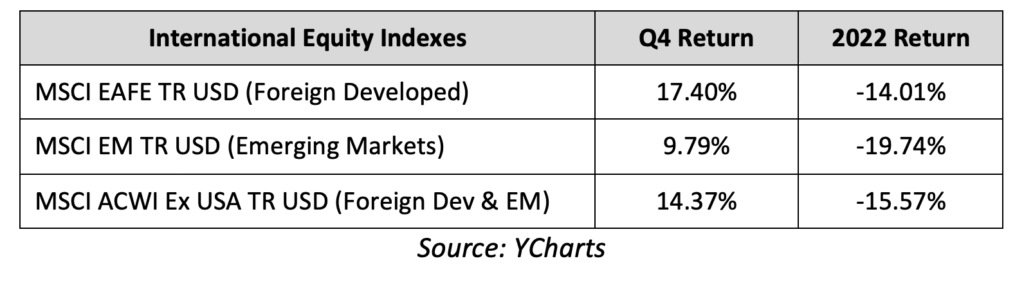

Internationally, foreign markets handily outperformed the S&P 500 in the fourth quarter thanks to a large bounce in Chinese stocks as Beijing ended its “Zero-Covid” policy and commenced an economic reopening, while a falling dollar boosted global economic sentiment. Foreign developed markets outperformed emerging markets in the fourth quarter thanks in part to a large bounce in U.K. shares following the resignation of PM Truss and the abandonment of her fiscal spending and tax cut plan. For the full-year 2022, foreign developed markets registered solidly negative returns, but thanks to the fourth-quarter rally, relatively outperformed the S&P 500.

The leading benchmark for bonds (Bloomberg Barclays US Aggregate Bond Index) realized a positive return for the fourth quarter but declined sharply for the full year of 2022, as more-aggressive-than-expected Fed rate hikes combined with decades-high inflation pressured most bond classes.

Looking deeper into the fixed income markets, longer-duration bonds outperformed those with shorter durations in the fourth quarter, as bond investors reacted to more-resilient-than-expected economic data. For the full year, shorter-term bonds handily outperformed longer-duration bonds as they were less impacted by Fed rate hikes and spiking inflation.

Turning to the corporate bond market, both higher-yielding, lower-quality corporate bonds and investment grade bonds posted similarly positive returns for the fourth quarter, as investors reacted to the possible peak in inflation. Lower-yielding and safer investment-grade corporate debt underperformed for the full year, however, as investors shunned those bonds for shorter-duration debt and corporate debt with higher yields.

Q1 and 2023 Market Outlook

Markets ended 2022 on a decidedly negative note and the December losses helped to ensure that 2022 was the worst year for stocks since 2008 and the worst year for bonds in multiple decades, as both asset classes posted annual declines for the first time since the 1960s.

The losses in stocks and bonds were driven by decades-high inflation, a historic Fed rate hike campaign and geopolitical unrest. But while those factors were clear negatives for asset prices in 2022, it’s important to note that as we enter 2023, the market is approaching a potentially important transition period that could see each of these headwinds ease in the months ahead.

First, inflation has shown definitive signs of peaking and declining. The Consumer Price Index has fallen from a high of 9.1% in June to 7.1% in November, while other metrics of inflation have registered similar declines. Now, to be clear, inflation remains much too high in an absolute sense, but if price pressures ease faster than expected, that will present a positive surprise for markets in the first several months of 2023.

Second, after a historically aggressive rate hiking campaign in 2022, the current Fed hiking cycle is likely nearly complete. In December, the Federal Reserve signaled that it expected the peak interest rate to be just 75 basis points higher than the current rate. That level could easily be reached within the first few months of 2023 and the Fed ending its rate hike campaign will remove a significant headwind from asset prices.

Finally, while both economic growth and corporate earnings are expected to decline in 2023, those negative expectations have been at least partially priced into stocks and bonds at current levels. As such, if the economy or corporate America proves to be more resilient than forecasts, it could provide a positive spark for asset markets in early 2023.

As we start the new year, we should expect financial media commentary to be focused on the 2022 losses and current market risks, including earnings concerns and recession fears. But the market is a forward-looking instrument, and while there are undoubtedly economic and corporate challenges ahead in 2023, some of those best-known risks are partially priced into markets already, and the truth is that there are potential positive catalysts lurking as we start a new year.

More broadly, market history is clear: Declines of the magnitude we saw in 2022 are usually followed by strong recoveries, not further weakness. The S&P 500 hasn’t registered two consecutive negative years since 2002, while bonds, represented by the Bloomberg U.S. Aggregate Bond Index, have never experienced two negative consecutive years. And that reality underscores an important point, that market declines such as we witnessed in 2022 have ultimately yielded substantial long-term opportunities in both stocks and bonds.

The stagflation of the 1970s and sky-high interest rates of the early 1980s eventually gave way to the strong economic growth and market rally of the 1980s. The dot-com bubble burst of the early 2000s was followed by substantial market gains into the mid-2000s. The financial crisis, which remains the most dire economic situation we’ve experienced in modern market history, was followed by strong rallies in the years that followed, and not even the worst global pandemic in over 100 years could result in sustainably lower asset prices.

As such, while we are prepared for continued volatility and are focused on managing both risks and return potential, we understand that a well-planned, long-term-focused, and diversified financial plan can withstand virtually any market surprise and related bout of volatility, including multi-decade highs in inflation, historic Fed rate hikes, geopolitical unrest, and rising recession risks.

We understand the risks facing both the markets and the economy, and we are committed to helping you effectively navigate this challenging investment environment. Recent volatility is unlikely to alter a diversified approach appropriately set up to meet your long-term investment goals. A diversified approach will be based a portfolio allocation that considers your financial position, risk tolerance, and investment timeline. It’s important to stay invested, remain patient, and stick to the plan.